As Mortgage Rates for Jumbo Loans takes center stage, this opening passage beckons readers with engaging insights into the world of mortgage rates for jumbo loans. From defining jumbo loans to exploring current trends, this topic promises to provide valuable information for those navigating the realm of real estate financing.

In this discussion, we will delve into the intricacies of mortgage rates for jumbo loans, shedding light on how credit scores, down payments, and loan amounts impact these rates. Stay tuned to discover tips for finding the best rates and the advantages of working with a mortgage broker.

Mortgage Rates

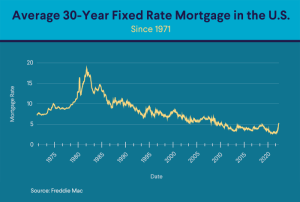

When you take out a mortgage to buy a home, you’ll encounter the term “mortgage rates.” These rates represent the interest you’ll pay on your loan. Lenders charge interest as a way to make a profit on the money they lend to you.

Mortgage rates are determined by a variety of factors, including:

Fixed-Rate Mortgages vs. Adjustable-Rate Mortgages

Fixed-rate mortgages have an interest rate that remains the same for the entire term of the loan. On the other hand, adjustable-rate mortgages (ARMs) have an interest rate that can change periodically, usually in relation to an index, which means your payments can go up or down.

While fixed-rate mortgages provide stability and predictability, adjustable-rate mortgages often start with lower initial rates, making them attractive to some borrowers. However, they come with the risk of increasing rates in the future.

Economic Factors Influencing Mortgage Rates

Economic factors play a significant role in determining mortgage rates. Some key factors include:

- The state of the economy: In a strong economy, interest rates may rise, leading to higher mortgage rates. Conversely, in a weak economy, rates may decrease.

- Inflation: Higher inflation typically leads to higher mortgage rates as lenders seek to offset the decrease in purchasing power caused by inflation.

- The Federal Reserve: The Federal Reserve’s monetary policy decisions can impact mortgage rates. For example, when the Fed raises interest rates, mortgage rates tend to increase as well.

Mortgage Rates for Jumbo Loans

When it comes to jumbo loans, they are loans that exceed the conforming loan limits set by the Federal Housing Finance Agency. These loans are typically used to finance high-priced properties and are considered non-conventional due to their size.

Differences from Conventional Loans

- Jumbo loans have higher credit score requirements compared to conventional loans.

- Down payment requirements are usually more substantial for jumbo loans.

- Interest rates for jumbo loans are typically higher than those for conventional loans.

Comparison of Mortgage Rates

Historically, mortgage rates for jumbo loans have been higher than rates for conventional loans. This is due to the increased risk associated with lending larger amounts of money. However, in recent years, the gap between jumbo loan rates and conventional loan rates has narrowed.

Current Trends

- Amidst the economic uncertainty caused by the global pandemic, mortgage rates for jumbo loans have seen some fluctuations.

- As the economy stabilizes and interest rates remain low, some lenders are offering competitive rates on jumbo loans to attract borrowers.

- Experts predict that mortgage rates for jumbo loans may continue to be influenced by market conditions and government policies in the coming months.

Factors Influencing Mortgage Rates for Jumbo Loans

When it comes to jumbo loans, several factors play a crucial role in determining the mortgage rates offered to borrowers. Understanding these factors can help individuals make informed decisions when considering a jumbo loan for their housing needs.

Credit Scores Impact on Mortgage Rates

Credit scores have a significant impact on the mortgage rates for jumbo loans. Lenders use credit scores to assess the risk associated with lending money to an individual. Borrowers with higher credit scores are seen as less risky and, therefore, may qualify for lower interest rates on their jumbo loans. On the other hand, individuals with lower credit scores may face higher interest rates or may even struggle to qualify for a jumbo loan.

Role of Down Payments in Jumbo Loan Rates

Down payments also play a crucial role in determining jumbo loan rates. A larger down payment typically results in a lower loan-to-value ratio, which can lead to lower interest rates. Lenders often offer better terms to borrowers who can make a substantial down payment, as it reduces the risk for the lender. Conversely, borrowers who make smaller down payments may face higher interest rates to compensate for the increased risk.

Loan Amount and Loan-to-Value Ratio Impact on Jumbo Loan Rates

The loan amount and loan-to-value ratio are key factors that influence jumbo loan rates. Generally, larger loan amounts and higher loan-to-value ratios pose greater risks for lenders, resulting in higher interest rates for borrowers. Lenders may offer more competitive rates to borrowers with lower loan amounts and lower loan-to-value ratios. It is essential for borrowers to consider these factors when applying for a jumbo loan to secure the best possible terms.

Finding the Best Mortgage Rates for Jumbo Loans

When looking for the best mortgage rates for jumbo loans, it’s essential to shop around and compare offers from different lenders. This process can help you secure a competitive rate that suits your financial situation and needs.

Tips on Shopping for Competitive Mortgage Rates for Jumbo Loans

- Check with multiple lenders to compare interest rates, fees, and terms for jumbo loans.

- Consider using online comparison tools to streamline the rate comparison process.

- Don’t forget to factor in additional costs like closing fees, points, and private mortgage insurance (PMI).

- Ask lenders about any special promotions or discounts that may apply to jumbo loans.

Importance of Comparing Offers from Different Lenders

- Comparing offers from different lenders can help you find the most competitive mortgage rates for jumbo loans.

- You can identify potential savings and negotiate better terms by exploring multiple options.

- Understanding the range of rates available in the market can empower you to make informed decisions.

Benefits of Working with a Mortgage Broker for Jumbo Loan Rates

- A mortgage broker can leverage their network of lenders to find competitive rates for jumbo loans on your behalf.

- Brokers may have access to exclusive deals and discounts that are not directly available to individual borrowers.

- Brokers can offer personalized guidance and support throughout the mortgage application process, helping you navigate complex jumbo loan requirements.

In conclusion, Mortgage Rates for Jumbo Loans offers a comprehensive guide to understanding and securing favorable rates in the competitive real estate market. Armed with knowledge about the factors influencing rates and strategies for finding the best deals, individuals can make informed decisions when pursuing jumbo loans.

Query Resolution

What are jumbo loans?

Jumbo loans are mortgages that exceed the conforming loan limits set by government-sponsored entities like Fannie Mae and Freddie Mac.

How do mortgage rates for jumbo loans differ from conventional loans?

Mortgage rates for jumbo loans are typically higher than rates for conventional loans due to the increased risk associated with larger loan amounts.

Why is it important to compare offers from different lenders?

Comparing offers from different lenders can help borrowers find the most competitive rates and terms for their jumbo loans, potentially saving them money in the long run.

What role does the loan amount play in determining jumbo loan rates?

The loan amount directly influences jumbo loan rates, with larger loan amounts often resulting in higher interest rates.

How can a mortgage broker assist in finding favorable jumbo loan rates?

A mortgage broker can leverage their industry connections and expertise to help borrowers navigate the complex landscape of jumbo loans, potentially securing better rates and terms.