Embark on a journey exploring the nuances of Fixed vs. Adjustable Mortgage Rates, where we unravel the complexities and benefits of each type to help you make an informed decision.

Delve into the realm of mortgage rates to understand the intricacies that could impact your financial future.

Fixed vs. Adjustable Mortgage Rates

When it comes to choosing a mortgage, one of the key decisions borrowers face is whether to opt for a fixed rate or an adjustable rate. Each type of rate has its own set of advantages and disadvantages, depending on the borrower’s financial situation and risk tolerance.

Fixed Mortgage Rates

Fixed mortgage rates are exactly as the name suggests – fixed. This means that the interest rate remains the same throughout the life of the loan, providing predictability and stability in monthly payments. Borrowers who prefer knowing exactly how much they will pay each month often opt for fixed rates.

Adjustable Mortgage Rates

On the other hand, adjustable mortgage rates fluctuate based on market conditions. Typically, these rates start lower than fixed rates, offering initial savings to borrowers. However, these rates can adjust periodically, leading to potential increases in monthly payments over time.

Comparing the Pros and Cons

- Fixed Rates:

- Pros: Predictable monthly payments, protection against rising interest rates.

- Cons: Usually higher initial rates compared to adjustable rates.

- Adjustable Rates:

- Pros: Lower initial rates, potential for lower payments if rates decrease.

- Cons: Uncertainty in future payments, risk of rates increasing over time.

Examples of Situations

Fixed rates are beneficial for borrowers who prioritize stability and want to lock in a rate for the long term. On the other hand, adjustable rates may be suitable for borrowers who plan to sell or refinance before the rates adjust, or those who expect interest rates to decrease in the future.

Factors Influencing Mortgage Rates

Several economic factors play a crucial role in determining mortgage rates. Understanding these factors can help borrowers make informed decisions when choosing between fixed and adjustable rates.

Economic Factors Impacting Mortgage Rates

1. Supply and Demand: Mortgage rates are influenced by the supply of credit available in the market and the demand from borrowers. When there is high demand for loans, interest rates tend to rise.

2. Economic Growth: Strong economic growth typically leads to higher mortgage rates as lenders seek to adjust rates to match the growing economy.

3. Housing Market Conditions: The state of the housing market, including home prices and sales, can impact mortgage rates. A robust housing market may lead to higher rates.

Inflation’s Impact on Fixed and Adjustable Rates

Inflation affects fixed and adjustable rates differently. Fixed rates are more sensitive to inflation since they lock in a specific rate for the entire loan term, protecting borrowers from rising inflation. On the other hand, adjustable rates can fluctuate with inflation, leading to potential increases in monthly payments for borrowers.

Federal Reserve Influence on Mortgage Rates

The Federal Reserve plays a significant role in influencing mortgage rates through its monetary policy decisions. When the Fed raises or lowers interest rates, it directly impacts mortgage rates. For instance, a rate hike by the Fed can lead to an increase in mortgage rates.

Credit Scores Impact on Mortgage Rates

Credit scores play a crucial role in determining the interest rate borrowers receive on their mortgage. A higher credit score typically results in a lower interest rate, as lenders view borrowers with good credit as less risky. On the other hand, borrowers with lower credit scores may face higher interest rates to compensate for the perceived risk.

Types of Fixed-Rate Mortgages

When it comes to fixed-rate mortgages, there are several types available to borrowers. Each type offers different terms and benefits, catering to various financial situations and preferences.

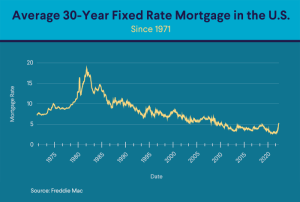

30-Year Fixed-Rate Mortgage

A 30-year fixed-rate mortgage is one of the most common options for homebuyers. With this type of loan, the interest rate remains the same for the entire 30-year term, providing stability and predictability in monthly payments.

15-Year Fixed-Rate Mortgage

A 15-year fixed-rate mortgage is another popular choice among borrowers. While the monthly payments are higher compared to a 30-year mortgage, the overall interest paid over the life of the loan is significantly lower. This type of mortgage allows borrowers to pay off their loan faster and build equity in their home more quickly.

20-Year Fixed-Rate Mortgage

A 20-year fixed-rate mortgage falls in between the 30-year and 15-year options in terms of monthly payments and total interest paid. This type of loan offers a shorter term than a 30-year mortgage but with more manageable monthly payments compared to a 15-year mortgage.

Advantages of a 15-Year Fixed-Rate Mortgage over a 30-Year One

- Lower total interest paid over the life of the loan

- Faster equity building in the home

- Shorter term means being debt-free sooner

When to Choose a Specific Type of Fixed-Rate Mortgage

- Opt for a 30-year fixed-rate mortgage for lower monthly payments and more flexibility.

- Consider a 15-year fixed-rate mortgage if you can afford higher monthly payments and want to save on interest in the long run.

- Choose a 20-year fixed-rate mortgage for a balance between the benefits of a 15-year and 30-year loan.

Types of Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) come in various types with different structures and features, offering flexibility to borrowers. Here are some common types of adjustable-rate mortgages:

1. Hybrid ARMs

Hybrid ARMs feature an initial fixed-rate period followed by adjustable rates. For example, a 5/1 ARM has a fixed rate for the first 5 years, then adjusts annually. This type offers lower initial rates but potential for higher payments later.

2. Interest-Only ARMs

Interest-only ARMs allow borrowers to pay only interest for a set period, typically 5-10 years, before principal payments begin. While initial payments are lower, they can increase significantly when principal payments kick in.

3. Payment Option ARMs

Payment option ARMs give borrowers flexibility to choose from various payment options each month. Options may include minimum payments, interest-only payments, or full principal and interest payments. However, choosing minimum payments can lead to negative amortization.

4. Cash Flow ARMs

Cash flow ARMs allow borrowers to adjust their payments based on their cash flow. This type offers flexibility to make lower payments during tight financial periods but can lead to higher payments later on.

5. Rate-Cap ARMs

Rate-cap ARMs limit how much the interest rate can increase each adjustment period or over the life of the loan. This provides some protection against sharp rate hikes but may also result in higher payments if rates rise significantly.

6. Option ARM

An Option ARM allows borrowers to choose from different payment options each month, including minimum payments, interest-only payments, and fully amortizing payments. This type of ARM offers flexibility but can also lead to negative amortization if minimum payments are selected.

7. Convertible ARMs

Convertible ARMs give borrowers the option to convert their adjustable-rate mortgage into a fixed-rate mortgage at certain points during the loan term. This provides a way to lock in a fixed rate if interest rates are expected to rise. These different types of adjustable-rate mortgages cater to varying borrower needs and risk tolerances. Understanding the features and risks associated with each type is crucial when considering an adjustable-rate mortgage.

In conclusion, the choice between Fixed and Adjustable Mortgage Rates is crucial and understanding the differences is key to securing a sound financial future.

Essential Questionnaire

What are the main differences between fixed and adjustable mortgage rates?

Fixed rates remain constant throughout the loan term, while adjustable rates fluctuate based on market conditions.

When is it advisable to choose a fixed-rate mortgage over an adjustable-rate one?

A fixed-rate mortgage is ideal for individuals seeking stability in monthly payments and protection against interest rate hikes.

What factors should be considered before deciding between fixed and adjustable rates?

Factors such as financial goals, risk tolerance, and market trends should be evaluated to make an informed decision.