Mortgage Rates and the Federal Reserve sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual formal language style and brimming with originality from the outset.

Exploring how mortgage rates are influenced by various factors, the role of the Federal Reserve in shaping these rates, and the overall impact on the economy provides a comprehensive view of this complex relationship.

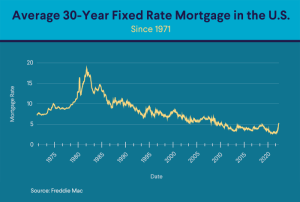

MORTGAGE RATES

When it comes to determining mortgage rates, several factors come into play that can influence the final rate offered to borrowers.

Factors Influencing Mortgage Rates

- Economic indicators: Factors like inflation, employment rates, and GDP can impact mortgage rates.

- Loan type: The type of loan (conventional, FHA, VA) and the borrower’s credit score can affect the rate.

- Market conditions: Supply and demand in the housing market can cause rates to fluctuate.

- Term length: The length of the loan term, whether 15, 20, or 30 years, can impact the interest rate.

Fixed-rate vs. Adjustable-rate Mortgages

Fixed-rate mortgages have a set interest rate for the entire loan term, providing stability in monthly payments. On the other hand, adjustable-rate mortgages (ARMs) have rates that can change periodically, based on market conditions, potentially leading to lower initial rates but higher uncertainty in the future.

FEDERAL RESERVE AND MORTGAGE RATES

The Federal Reserve plays a crucial role in influencing mortgage rates through its monetary policy decisions. By adjusting key interest rates, the Federal Reserve directly impacts the cost of borrowing for consumers seeking mortgages.When the Federal Reserve lowers the federal funds rate, which is the interest rate at which banks lend money to each other overnight, it can lead to a decrease in mortgage rates.

This is because lower federal funds rates often result in lower overall interest rates in the economy, making borrowing more affordable for homebuyers.Conversely, when the Federal Reserve raises the federal funds rate, it can cause mortgage rates to increase. Higher federal funds rates can translate to higher borrowing costs for banks, which in turn can lead to higher mortgage rates for consumers.

Impact of Federal Reserve Policies on Mortgage Rates

The Federal Reserve’s policies have a direct impact on mortgage rates, influencing the overall cost of borrowing for homeowners. Here are some key ways in which Federal Reserve decisions affect mortgage rates:

- When the Federal Reserve implements expansionary monetary policy by lowering interest rates, mortgage rates tend to decrease, stimulating borrowing and economic activity.

- Conversely, during periods of contractionary monetary policy where the Federal Reserve raises interest rates to combat inflation, mortgage rates typically rise, making borrowing more expensive.

- The Federal Reserve’s communication and guidance regarding future policy actions also play a role in shaping market expectations, which can impact mortgage rates even before official policy changes are made.

Comparing Historical Trends of Mortgage Rates with Federal Reserve Decisions

Looking back at historical data, there is a clear correlation between Federal Reserve decisions and mortgage rates. For example, during the financial crisis of 2008, the Federal Reserve implemented aggressive rate cuts to stimulate the economy, leading to record-low mortgage rates.Similarly, in recent years, the Federal Reserve’s gradual increase in interest rates has contributed to the uptick in mortgage rates observed in the market.

By analyzing the historical relationship between Federal Reserve policies and mortgage rates, we can gain insights into how these two factors interact to shape the housing market and overall economy.

ECONOMIC INDICATORS

Understanding the key economic indicators that impact mortgage rates is crucial for homeowners and potential buyers. These indicators provide valuable insights into the overall health of the economy and help predict potential changes in mortgage rates.

Employment Rates and Mortgage Rates

Employment rates play a significant role in influencing mortgage rates. When the job market is strong and unemployment rates are low, it indicates a healthy economy. Lenders are more confident in borrowers’ ability to repay loans, leading to lower mortgage rates. Conversely, high unemployment rates can signal economic instability, causing lenders to increase rates to mitigate the risk of defaults.

Inflation and Mortgage Rates

Inflation is another crucial factor that affects mortgage rates. When inflation rises, the purchasing power of currency decreases, leading to higher prices for goods and services. To combat the effects of inflation, lenders may raise mortgage rates to maintain profitability. Conversely, low inflation rates can result in lower mortgage rates as lenders adjust to the reduced cost of borrowing.

MORTGAGE RATE FORECAST

When it comes to predicting mortgage rate trends, experts rely on a combination of economic indicators, market analysis, and geopolitical events. These factors can influence whether rates will rise, fall, or remain stable in the near future.

Expert Predictions

- Many financial analysts predict that mortgage rates will gradually increase over the next few months. This forecast is based on the Federal Reserve’s plans to gradually raise interest rates to combat inflation.

- Some experts believe that geopolitical events, such as trade disputes or political instability, could lead to fluctuations in mortgage rates. Uncertainty in global markets can cause investors to seek safer investments, which could impact interest rates.

- Overall, the consensus among experts is that mortgage rates are likely to trend upwards in the coming year. Borrowers may want to consider locking in a rate sooner rather than later to take advantage of current low rates.

In conclusion, Mortgage Rates and the Federal Reserve shed light on the intricate dynamics between economic indicators, Federal Reserve policies, and mortgage rate forecasting. This discussion serves as a valuable resource for understanding the nuances of this crucial aspect of the financial landscape.

Answers to Common Questions

What factors can influence mortgage rates?

Factors such as economic indicators, inflation rates, and Federal Reserve policies can all play a role in determining mortgage rates.

How do Federal Reserve decisions affect mortgage rates?

The Federal Reserve’s decisions can impact mortgage rates by influencing overall interest rates and market conditions.

Can geopolitical events affect mortgage rate forecasts?

Yes, geopolitical events can introduce uncertainty into the market, leading to fluctuations in mortgage rate forecasts.