Delve into the reasons driving the surge in mortgage rates, from economic influences to historical comparisons, all leading to a deeper understanding of this pressing issue.

Why Are Mortgage Rates Rising?

As mortgage rates continue to climb, it is essential to understand the factors driving this increase. Several key elements contribute to the rise in mortgage rates, including economic indicators and historical trends.

Factors Influencing Mortgage Rate Increases

There are several factors influencing the rise in mortgage rates:

- Economic Growth: Strong economic growth can lead to higher inflation, prompting the Federal Reserve to raise interest rates, including those for mortgages.

- Inflation: Rising inflation erodes the purchasing power of the dollar, causing lenders to demand higher interest rates to compensate for the decrease in real returns.

- Market Demand: Increased demand for mortgages, coupled with limited housing supply, can push rates higher due to competition among borrowers.

Impact of Economic Indicators on Mortgage Rates

Economic indicators play a crucial role in determining mortgage rates:

- Unemployment Rate: A low unemployment rate signifies a strong economy, potentially leading to higher mortgage rates to curb inflation.

- GDP Growth: Robust GDP growth can fuel inflation, prompting the Federal Reserve to increase interest rates and subsequently affect mortgage rates.

- Consumer Price Index (CPI): The CPI measures changes in the cost of living, influencing inflation expectations and, consequently, mortgage rates.

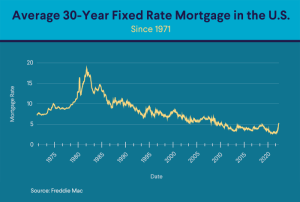

Comparing Historical Data to Current Trends

By comparing historical data to current trends, we can better understand the reasons behind rising mortgage rates:

- Historically Low Rates: Following the 2008 financial crisis, mortgage rates reached historic lows, but recent economic growth and inflation concerns have led to an upward trajectory.

- Rate Volatility: Mortgage rates can fluctuate based on market conditions, investor sentiment, and global economic factors, making it essential to monitor trends for informed decision-making.

MORTGAGE RATES

When it comes to purchasing a home, mortgage rates play a crucial role in determining the overall cost of borrowing money to buy a property. Mortgage rates refer to the interest rate charged on a mortgage loan, influencing how much you will pay each month to repay the borrowed amount.

These rates are determined by a combination of factors, including the current state of the economy, inflation rates, the Federal Reserve’s monetary policy, and the overall demand for loans. Lenders also take into account an individual’s credit score, down payment amount, and loan term when setting mortgage rates.

Relationship between Mortgage Rates and the Broader Economy

Mortgage rates are closely tied to the broader economy. When the economy is strong and inflation is low, mortgage rates tend to rise as lenders seek higher returns on their investments. Conversely, during economic downturns or periods of low inflation, mortgage rates may decrease to stimulate borrowing and spending.

For example, during times of economic growth, the Federal Reserve may raise interest rates to prevent inflation from rising too quickly. This can lead to an increase in mortgage rates, making it more expensive for borrowers to take out loans and potentially slowing down the real estate market.

Impact of Mortgage Rates on Home Affordability and the Real Estate Market

- Mortgage rates directly impact the affordability of homes, as higher rates mean higher monthly mortgage payments for buyers. This can price some potential buyers out of the market or force them to settle for less expensive properties.

- Lower mortgage rates, on the other hand, can make homeownership more accessible by reducing monthly payments and increasing purchasing power. This can lead to an increase in demand for homes and drive up real estate prices.

- Fluctuations in mortgage rates can also affect the refinance market, as homeowners may choose to refinance their existing mortgages to take advantage of lower rates, freeing up additional funds for other expenses or investments.

In conclusion, the complexities of mortgage rate fluctuations are unraveled, shedding light on the pivotal role they play in shaping the real estate landscape and beyond.

Top FAQs

What factors are driving the increase in mortgage rates?

The rise in mortgage rates can be attributed to various factors such as economic conditions, inflation, and market demand.

How do mortgage rates impact home affordability?

Mortgage rates directly affect home affordability, as higher rates can make monthly payments more expensive for buyers.