Beginning with Mortgage Rates by Credit Score, the narrative unfolds in a compelling and distinctive manner, drawing readers into a story that promises to be both engaging and uniquely memorable.

Exploring the relationship between credit scores and mortgage rates reveals crucial insights for borrowers looking to make informed decisions about their home loans.

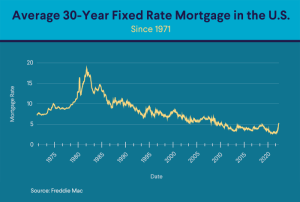

MORTGAGE RATES

Mortgage rates refer to the interest charged on a mortgage loan. These rates have a significant impact on borrowers as they determine the overall cost of borrowing money to purchase a home.Fixed-rate mortgages have a set interest rate that remains constant throughout the loan term, providing borrowers with predictability and stability in their monthly payments. On the other hand, adjustable-rate mortgages (ARMs) have interest rates that can fluctuate based on market conditions, potentially leading to lower initial rates but higher risks of payment increases in the future.

Comparison of Fixed-Rate Mortgages and Adjustable-Rate Mortgages

- Fixed-rate mortgages offer consistency in monthly payments, making budgeting easier for borrowers, while adjustable-rate mortgages can provide lower initial rates but may increase over time.

- Fixed-rate mortgages are ideal for borrowers who prioritize stability and predictability, while adjustable-rate mortgages may be suitable for those planning to sell or refinance before potential rate adjustments.

- Economic factors such as inflation, economic growth, and the Federal Reserve’s monetary policy can influence mortgage rates for both fixed-rate and adjustable-rate mortgages.

MORTGAGE RATES BY CREDIT SCORE

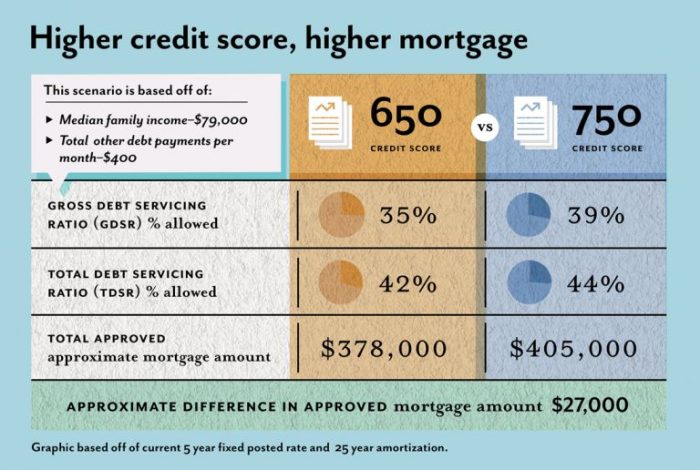

Credit scores play a significant role in determining the mortgage rates that borrowers are eligible for. Lenders use credit scores as a measure of an individual’s creditworthiness, with higher scores typically resulting in lower interest rates.Having a good credit score can lead to lower mortgage rates, saving borrowers money over the life of the loan. On the other hand, lower credit scores can result in higher interest rates, making homeownership more expensive.

Typical Interest Rates for Different Credit Score Ranges

- Credit Score 760 and above: Borrowers with credit scores of 760 or higher usually qualify for the best interest rates available, often receiving the lowest rates on the market.

- Credit Score 700-759: This range is considered good, and borrowers can still secure competitive interest rates, although they may be slightly higher than those with scores above 760.

- Credit Score 620-699: Borrowers in this range may still be approved for mortgages, but they are likely to face higher interest rates due to the increased risk perceived by lenders.

- Credit Score below 620: Individuals with credit scores below 620 may have difficulty qualifying for a mortgage, and if approved, they can expect significantly higher interest rates.

Improving your credit score by even a few points can make a significant difference in the mortgage rate you qualify for.

Strategies for Improving Credit Scores to Secure Better Mortgage Rates

- Make payments on time: Payment history is a key factor in credit scores, so ensuring timely payments on all debts is crucial.

- Reduce credit card balances: Lowering credit card balances can help improve credit utilization ratios, positively impacting credit scores.

- Avoid opening new credit accounts: Opening multiple new accounts can lower the average age of credit history, potentially lowering credit scores.

- Regularly check credit reports: Monitoring credit reports for errors and addressing any issues promptly can help maintain or improve credit scores.

CREDIT SCORE RANGES

Having a good credit score is essential when it comes to getting favorable mortgage rates. Lenders use credit scores to evaluate the risk of lending money to a borrower, with lower credit scores typically resulting in higher interest rates.

Poor Credit Score Range

- Borrowers with poor credit scores, typically below 580, may struggle to qualify for a mortgage.

- Those with poor credit scores may face higher interest rates, which can significantly increase monthly mortgage payments.

- Lenders may require a larger down payment to offset the risk associated with poor credit scores.

Fair Credit Score Range

- Credit scores in the fair range, usually between 580 and 669, may qualify for a mortgage but at higher interest rates.

- Borrowers in this range can expect to pay more in interest compared to those with good or excellent credit scores.

- Monthly mortgage payments for borrowers in the fair credit range may be higher due to increased interest rates.

Good Credit Score Range

- With credit scores ranging from 670 to 739, borrowers can access more competitive mortgage rates.

- Individuals with good credit scores are likely to secure lower interest rates, resulting in lower monthly mortgage payments.

- Lenders may offer better terms and lower fees to borrowers with good credit scores.

Excellent Credit Score Range

- Borrowers with excellent credit scores, typically above 740, are considered low-risk by lenders.

- Individuals in this credit score range can access the lowest mortgage rates available.

- Monthly mortgage payments for those with excellent credit scores are usually the lowest due to the favorable interest rates offered.

SHOPPING AROUND FOR MORTGAGE RATES

When looking for a mortgage, it’s essential to shop around and compare rates from different lenders. This can help you find the best deal that suits your financial situation. Here are some tips on how to effectively compare mortgage rates:

Comparing Mortgage Rates

- Research online: Look at various lenders’ websites, use comparison tools, and check for current rates.

- Contact multiple lenders: Reach out to different banks, credit unions, and mortgage brokers to get quotes.

- Consider different loan types: Compare rates for fixed-rate mortgages, adjustable-rate mortgages, and other loan options.

- Look beyond the interest rate: Consider additional fees, closing costs, and the overall terms of the loan.

Importance of Getting Pre-Approved

- Getting pre-approved for a mortgage can give you a clearer picture of how much you can borrow.

- Pre-approval can also show sellers that you are a serious buyer, potentially giving you an edge in a competitive market.

- Having a pre-approval can help you lock in a rate and avoid any surprises later in the process.

Step-by-Step Guide to Shopping Around

- Check your credit score and financial situation.

- Research and compare rates online from different lenders.

- Reach out to lenders for personalized quotes and information.

- Provide necessary documents for pre-approval and compare offers.

- Negotiate terms, ask questions, and make an informed decision based on your needs.

In conclusion, understanding how credit scores influence mortgage rates can empower individuals to take proactive steps towards securing favorable loan terms and achieving their homeownership dreams.

Questions Often Asked

How do credit scores impact mortgage rates?

Credit scores play a significant role in determining the interest rates offered on mortgages. A higher credit score typically results in lower rates, while a lower score may lead to higher rates.

What are some strategies for improving credit scores to get better mortgage rates?

Strategies like paying bills on time, keeping credit card balances low, and monitoring credit reports for errors can help improve credit scores over time, leading to better mortgage rates.

Why is it important to get pre-approved for a mortgage?

Getting pre-approved for a mortgage can give you a clear idea of how much you can borrow and the interest rate you qualify for, helping you shop for homes within your budget.