Embark on a journey through the intricate world of Mortgage Rate Trends in the US, exploring historical data and factors that drive fluctuations in rates.

Discover how economic indicators and regional variations play a crucial role in shaping mortgage rates, providing a comprehensive understanding of this dynamic market.

MORTGAGE RATE TRENDS IN THE US

Mortgage rates play a crucial role in the US real estate market, impacting the affordability of homes for buyers and influencing the overall housing market dynamics. Understanding the trends in mortgage rates is essential for both homeowners and potential buyers.

Historical Data on Mortgage Rate Trends

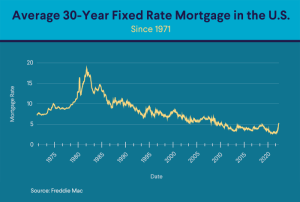

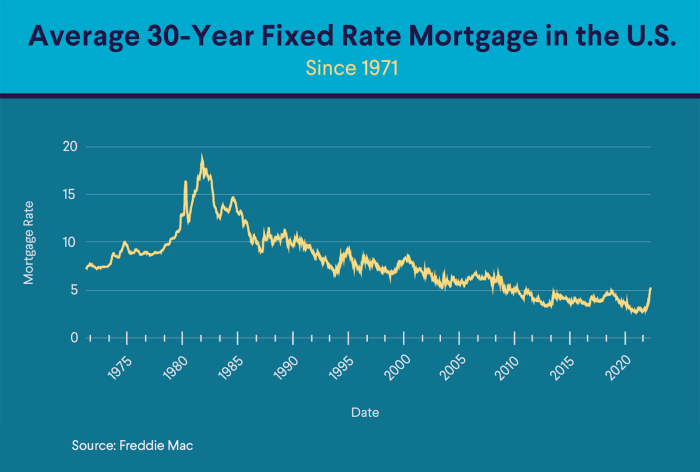

- Over the past decade, mortgage rates in the US have experienced significant fluctuations. In 2010, the average rate for a 30-year fixed-rate mortgage was around 4.69%, dropping to historic lows below 3% in 2020 due to economic conditions and the impact of the COVID-19 pandemic.

- However, in recent years, mortgage rates have started to climb back up, reaching around 3.5% to 4% in 2021 and continuing to rise in 2022.

Factors Influencing Fluctuations in Mortgage Rates

- The Federal Reserve’s monetary policy decisions, economic indicators such as inflation and employment rates, and global economic events all play a role in determining mortgage rates.

- Market conditions, investor demand for mortgage-backed securities, and government policies also influence the direction of mortgage rates in the US.

Comparison of Current Mortgage Rates

- As of [current date], the average rate for a 30-year fixed-rate mortgage in the US is around [current rate]%, which is higher compared to the rates seen in the past few years but still relatively low historically.

- Analysts predict that mortgage rates may continue to rise in the coming months, impacting affordability for homebuyers and potentially slowing down the housing market activity.

IMPACT OF ECONOMIC INDICATORS ON MORTGAGE RATES

Economic indicators play a crucial role in determining the direction of mortgage rates in the US. Various factors such as inflation rates, GDP growth, Federal Reserve’s monetary policy decisions, employment data, consumer spending, and global economic events can all influence the movement of mortgage rates.

Inflation Rates and GDP Growth

Inflation rates and GDP growth are key economic indicators that can impact mortgage rates. When inflation is high, lenders may increase interest rates to offset the decrease in purchasing power. Similarly, strong GDP growth can lead to higher mortgage rates as lenders anticipate a stronger economy.

Federal Reserve’s Monetary Policy Decisions

The Federal Reserve plays a significant role in setting the tone for mortgage rates through its monetary policy decisions. When the Fed decides to raise interest rates, mortgage rates tend to follow suit. Conversely, when the Fed cuts rates to stimulate the economy, mortgage rates may decrease.

Employment Data and Consumer Spending

Employment data and consumer spending also impact mortgage rates. A strong job market and increased consumer spending can signal a healthy economy, leading to higher mortgage rates. On the other hand, rising unemployment rates or a decrease in consumer spending may result in lower mortgage rates.

Global Economic Events

Global economic events can have a ripple effect on mortgage rate trends in the US. Events such as trade agreements, geopolitical tensions, or economic crises in other countries can cause investors to seek safe-haven assets like US Treasury bonds, which can lead to lower mortgage rates in the US.

TYPES OF MORTGAGE RATES

In the realm of mortgages, there are various types of rates that borrowers can choose from based on their financial goals and risk tolerance. Understanding the differences between fixed-rate and adjustable-rate mortgages, government-backed loans like FHA and VA mortgages, jumbo mortgage rates, and conventional mortgage rates is crucial for making informed decisions in the real estate market.

Fixed-Rate vs. Adjustable-Rate Mortgages

Fixed-rate mortgages offer stable interest rates throughout the loan term, providing predictability for budgeting purposes. On the other hand, adjustable-rate mortgages have interest rates that can fluctuate based on market conditions, typically starting with a lower rate that adjusts periodically. The trends for fixed-rate mortgages are influenced by long-term economic indicators, while adjustable-rate mortgages are more responsive to short-term economic changes.

Government-Backed Loans: FHA and VA Mortgages

Government-backed loans like FHA and VA mortgages cater to specific groups of borrowers, such as first-time homebuyers and veterans, offering competitive interest rates and lower down payment requirements. The rate trends for FHA and VA mortgages are influenced by government policies, economic conditions, and the overall housing market dynamics.

Jumbo Mortgage Rates vs. Conventional Mortgage Rates

Jumbo mortgage rates are higher than conventional mortgage rates due to the larger loan amounts that exceed the conforming loan limits set by government-sponsored entities like Fannie Mae and Freddie Mac. The trends for jumbo mortgage rates may vary based on the performance of the luxury real estate market and the overall economic climate, while conventional mortgage rates are more closely tied to broad economic indicators and monetary policies.

Refinancing and Changing Mortgage Rate Trends

Refinancing involves replacing an existing mortgage with a new loan to take advantage of lower interest rates or better terms. Changing mortgage rate trends can impact the decision to refinance, as borrowers aim to secure more favorable rates to reduce monthly payments or shorten the loan term. The refinancing process is sensitive to shifts in mortgage rates, as borrowers monitor market trends to make strategic financial choices.

REGIONAL VARIATIONS IN MORTGAGE RATE TRENDS

When it comes to mortgage rate trends in the US, it’s important to understand that these rates can vary significantly from one region to another. Several factors contribute to these regional variations, including local housing market conditions, population growth, and job markets.Local housing market conditions play a crucial role in determining mortgage rate fluctuations. In areas where there is high demand for housing but limited supply, mortgage rates tend to be higher to reflect the increased risk for lenders.

On the other hand, in regions where there is an oversupply of housing, mortgage rates may be lower to attract potential buyers.Population growth also has a significant impact on regional mortgage rate trends. Rapid population growth can put pressure on the housing market, leading to higher mortgage rates. Conversely, areas with declining populations may experience lower mortgage rates as demand for housing decreases.The job market is another key factor that influences regional mortgage rate trends.

Strong job markets with low unemployment rates can lead to higher mortgage rates, as more people are able to afford homes. Conversely, regions with struggling job markets may see lower mortgage rates to stimulate the housing market.When comparing mortgage rate trends between urban and rural areas, it’s important to consider the driving factors behind these differences. Urban areas tend to have higher demand for housing, which can lead to higher mortgage rates.

Additionally, factors such as land scarcity and higher construction costs in urban areas can also contribute to higher rates. On the other hand, rural areas may have lower mortgage rates due to lower demand and lower costs of living.

Differences in Mortgage Rate Trends between States

- States with booming economies and high demand for housing may have higher mortgage rates.

- States with stable job markets and low population growth may experience lower mortgage rates.

- Geographic factors such as coastal regions or major metropolitan areas can also impact mortgage rates.

In conclusion, Mortgage Rate Trends in the US offer insights into the past, present, and potential future of the real estate market, highlighting the interconnected nature of economic indicators and regional influences on mortgage rates.

Question & Answer Hub

How do economic indicators affect mortgage rates?

Economic indicators such as inflation rates and GDP growth can impact mortgage rates by influencing market conditions and investor sentiment.

What are the differences between fixed-rate and adjustable-rate mortgages?

Fixed-rate mortgages have stable interest rates, while adjustable-rate mortgages have rates that can change over time based on market conditions.

How do regional variations impact mortgage rate trends?

Regional variations can be influenced by factors like local housing market conditions, population growth, and job markets, leading to differences in mortgage rate trends across states and areas.