Current Mortgage Rates 2024 sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual formal language style and brimming with originality from the outset.

Mortgage rates play a crucial role in the real estate market, affecting both buyers and sellers. Understanding the dynamics of current mortgage rates for 2024 is essential for making informed financial decisions. Let’s delve into the intricacies of how these rates are determined, their potential trends, and the impact they have on homebuyers’ purchasing power.

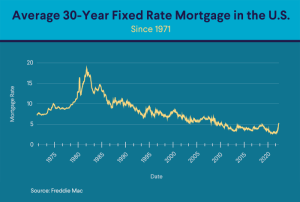

Overview of Current Mortgage Rates 2024

Mortgage rates refer to the interest charged on a mortgage loan used to purchase a home or refinance an existing mortgage. These rates can have a significant impact on the overall cost of borrowing and the monthly payments a homeowner makes.Understanding current mortgage rates for 2024 is crucial for individuals looking to buy a home or refinance their existing mortgage.

The rates can vary depending on economic conditions, market trends, and other factors. By staying informed about the current rates, borrowers can make informed decisions about when to lock in a rate and secure a favorable loan.

Factors Influencing Mortgage Rates

- The Federal Reserve: The Federal Reserve’s monetary policy decisions can directly impact mortgage rates. When the Fed raises or lowers interest rates, it can influence the direction of mortgage rates.

- Economic Indicators: Factors like inflation, unemployment rates, and GDP growth can also affect mortgage rates. Strong economic data may lead to higher rates, while weaker economic indicators could result in lower rates.

- Housing Market Trends: Supply and demand in the housing market can impact mortgage rates. A strong demand for homes may lead to higher rates, while a surplus of available homes could result in lower rates.

- Credit Score: Borrowers with higher credit scores are typically offered lower mortgage rates, as they are considered less risky by lenders.

Trends and Predictions

The current trends in mortgage rates leading into 2024 have been relatively stable, with rates hovering around historic lows. However, as the economy continues to recover from the impacts of the pandemic, there are several factors that could potentially influence mortgage rates in the upcoming year.

Impact of Inflation

Inflation is a key factor that could impact mortgage rates in 2024. As the Federal Reserve aims to combat rising inflation by potentially increasing interest rates, this could lead to a gradual uptick in mortgage rates throughout the year.

Housing Market Trends

The housing market plays a significant role in determining mortgage rates. With high demand for housing and limited inventory, mortgage rates may be influenced by the overall health of the housing market in 2024. Any shifts in supply and demand dynamics could impact mortgage rates accordingly.

Economic Growth and Federal Reserve Policy

The overall economic growth trajectory and Federal Reserve policy decisions will also play a crucial role in shaping mortgage rate trends in 2024. Depending on the pace of economic recovery and the Fed’s actions, mortgage rates could either remain stable or experience fluctuations throughout the year.

Global Events and Geopolitical Factors

External factors such as global events, geopolitical tensions, and international economic conditions can also impact mortgage rates. Any significant developments on the global stage could lead to changes in investor sentiment and market volatility, influencing mortgage rates in the process.

Comparing Mortgage Rates Across Lenders

When it comes to securing a mortgage, comparing rates across different lenders is crucial. This can potentially save you thousands of dollars over the life of your loan and ensure that you are getting the best deal possible for your financial situation.

Importance of Comparing Mortgage Rates

- Helps you find the lowest interest rate: By comparing rates from multiple lenders, you can identify the one offering the lowest interest rate, which can result in significant savings over time.

- Allows you to assess different loan terms: Each lender may offer different loan terms, such as fixed-rate or adjustable-rate mortgages. By comparing these options, you can choose the one that aligns best with your financial goals.

- Gives you negotiating power: When you have multiple rate quotes in hand, you have more leverage to negotiate with lenders and potentially secure a better deal.

Guide on How to Effectively Compare Mortgage Rates

- Research multiple lenders: Start by researching and obtaining rate quotes from various lenders, including banks, credit unions, and online lenders.

- Compare APRs: Look beyond the interest rate and consider the annual percentage rate (APR), which includes additional fees and charges associated with the loan.

- Consider loan terms: Evaluate the different loan terms offered by each lender, such as the duration of the loan and whether it’s a fixed or adjustable-rate mortgage.

- Review closing costs: Factor in closing costs when comparing rates, as these can significantly impact the overall cost of the loan.

Benefits of Securing the Best Mortgage Rate

- Lower monthly payments: A lower interest rate can lead to lower monthly mortgage payments, freeing up more of your income for other expenses.

- Reduced overall cost: Securing the best mortgage rate can result in substantial savings over the life of the loan, allowing you to build equity faster.

- Financial stability: By securing a favorable rate, you can ensure that your mortgage remains affordable, even if interest rates rise in the future.

Understanding the Impact of Mortgage Rates on Homebuyers

When it comes to purchasing a home, mortgage rates play a crucial role in determining the overall affordability for homebuyers. Fluctuations in mortgage rates can significantly impact how much a buyer can afford and the total cost of homeownership.

Effect on Purchasing Power

Mortgage rates directly affect homebuyers’ purchasing power. Higher interest rates mean higher monthly mortgage payments, which can reduce the amount of loan a buyer qualifies for. On the other hand, lower rates can make homes more affordable and increase purchasing power.

Strategies for Navigating Fluctuating Rates

- Monitor the market: Stay informed about current mortgage rates and market trends to make informed decisions.

- Lock in rates: Consider locking in a rate when it’s favorable to secure a lower interest rate for a set period.

- Improve credit score: A higher credit score can help you qualify for better rates and save money over the life of the loan.

Impact on Homebuyers

For example, let’s say a homebuyer is looking to purchase a $300,000 home with a 20% down payment. If the mortgage rate increases by 1%, their monthly mortgage payment could go up by hundreds of dollars, making the home less affordable or forcing them to look for a cheaper property.

As we wrap up our exploration of Current Mortgage Rates 2024, it becomes evident that staying informed about these rates is key to navigating the real estate landscape effectively. By keeping an eye on trends, making informed comparisons, and understanding the implications on homebuyers, individuals can make sound financial choices in the ever-changing market.

Commonly Asked Questions

How do I compare mortgage rates effectively?

To compare mortgage rates effectively, gather quotes from multiple lenders, consider the loan terms, assess any additional fees, and calculate the overall cost over the life of the loan.

What factors influence mortgage rates?

Mortgage rates are influenced by economic indicators, inflation rates, the housing market conditions, and the overall state of the economy.

Can external factors impact mortgage rates?

External factors like government policies, global economic trends, and geopolitical events can impact mortgage rates, causing them to fluctuate.