Exploring the intricate relationship between inflation and mortgage rates, this overview delves into the impact of economic factors on borrowing costs, providing a compelling narrative for readers.

It also sheds light on historical trends, borrower strategies, and forecasting methods in a clear and concise manner.

Impact of Inflation on Mortgage Rates

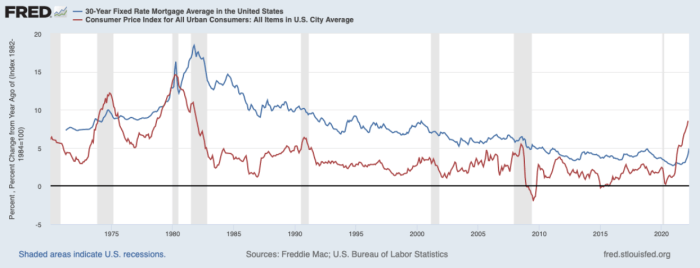

Inflation plays a significant role in determining the interest rates on mortgages. As inflation rises, the purchasing power of currency decreases, leading to an increase in the cost of goods and services. This rise in prices also affects borrowing costs, including mortgage rates.

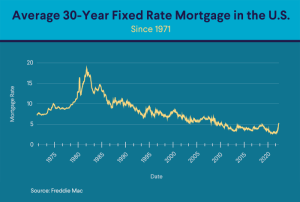

Historical Trends

- Historically, there has been a strong correlation between inflation rates and mortgage rates. When inflation is high, lenders demand higher interest rates to compensate for the decreased value of money over time.

- For example, during periods of high inflation in the 1970s and early 1980s, mortgage rates soared to double-digit levels to offset the effects of rising prices.

Relationship with Fixed-Rate Mortgages

- Fixed-rate mortgages are closely tied to inflation expectations. Lenders factor in inflation forecasts when setting interest rates for fixed-rate mortgages to ensure they earn a real return on their loans.

- When inflation expectations are high, lenders may increase mortgage rates to protect against the erosion of the loan’s value over time. Conversely, when inflation expectations are low, mortgage rates may decrease to attract borrowers.

Factors Influencing Mortgage Rates

When it comes to determining mortgage rates, several key factors play a crucial role in influencing the overall lending environment. Understanding these factors can help borrowers make informed decisions about their home loans.

Economic Indicators Impact

- The Gross Domestic Product (GDP) Growth: A strong GDP growth often leads to higher mortgage rates as it indicates a robust economy. Lenders may increase rates to match the demand for borrowing.

- Unemployment Rates: High unemployment rates can result in lower mortgage rates, as central banks may lower interest rates to stimulate economic growth and encourage borrowing.

- Inflation: Inflation can have a significant impact on mortgage rates. When inflation is high, lenders may raise rates to offset the decrease in the purchasing power of the currency.

Federal Reserve’s Monetary Policy

The Federal Reserve plays a pivotal role in influencing mortgage rates through its monetary policy decisions. When the Fed raises the federal funds rate, which is the rate at which banks lend to each other overnight, it can lead to an increase in mortgage rates. Conversely, when the Fed cuts rates to stimulate economic activity, mortgage rates may decrease as well.

Effects of Inflation on Borrowers

When it comes to inflation, borrowers need to consider how it impacts their purchasing power and mortgage payments. Let’s explore the various effects inflation can have on borrowers and how they can navigate through these challenges.

Impact on Purchasing Power

- Inflation reduces the purchasing power of borrowers as the value of money decreases over time. This means that borrowers may find it more challenging to afford the same goods and services, including mortgage payments.

- As inflation rises, borrowers may need to allocate a larger portion of their income towards mortgage payments, leaving less room for other expenses or savings.

Strategies to Mitigate Effects

- One strategy borrowers can use to mitigate the effects of inflation on their mortgage payments is to consider refinancing their mortgage to take advantage of lower interest rates.

- Another approach is to make extra payments towards the principal of the mortgage, which can help reduce the overall interest paid over time and shorten the loan term.

- Budgeting and planning for potential increases in mortgage payments due to inflation can also help borrowers stay on track and avoid financial strain.

Impact on Adjustable-Rate Mortgages vs. Fixed-Rate Mortgages

- Adjustable-rate mortgages (ARMs) are directly impacted by inflation since their interest rates can fluctuate based on market conditions. In times of high inflation, borrowers with ARMs may see their monthly payments increase.

- On the other hand, fixed-rate mortgages offer stable monthly payments throughout the loan term, providing borrowers with predictability and protection against inflation-induced interest rate hikes.

- Borrowers who are concerned about inflation and its impact on their mortgage payments may opt for a fixed-rate mortgage to lock in a consistent rate and avoid potential payment shocks.

Forecasting Mortgage Rate Trends

Forecasting mortgage rate trends is a crucial aspect of financial planning for both borrowers and lenders. Economists and analysts utilize various methods to predict future mortgage rate movements based on a combination of economic indicators, market trends, and government policies.

Methods Used for Forecasting Mortgage Rates

When it comes to predicting mortgage rate trends, experts often rely on the following methods:

- Analysis of economic data such as inflation rates, GDP growth, and employment figures.

- Monitoring of bond yields, particularly the 10-year Treasury yield, which serves as a benchmark for mortgage rates.

- Assessment of Federal Reserve policies and statements, as central bank decisions can impact interest rates.

Challenges in Predicting Mortgage Rate Movements

Predicting mortgage rate movements can be challenging, especially in an inflationary environment where economic conditions are constantly evolving. Some of the challenges include:

- Unforeseen changes in inflation rates or economic indicators that may lead to unexpected shifts in mortgage rates.

- Market volatility and external events such as geopolitical tensions or natural disasters that can impact investor confidence and interest rates.

- The interconnected nature of global economies, where developments in other countries can influence interest rates domestically.

External Factors Influencing Mortgage Rate Forecasts

External factors play a significant role in shaping mortgage rate forecasts. Global economic conditions, in particular, can have a profound impact on interest rates. For example:

- Global economic slowdowns or recessions may prompt central banks to lower interest rates, leading to a decrease in mortgage rates.

- Trade tensions between major economies can create uncertainty in financial markets, causing investors to seek safe-haven assets like bonds and driving down mortgage rates.

- Changes in commodity prices or currency values can also influence mortgage rates, as they reflect broader economic trends and investor sentiment.

In conclusion, the discussion highlights the importance of understanding inflation’s effects on mortgage rates and offers insights into navigating this complex financial landscape.

FAQ Insights

How does inflation directly influence mortgage rates?

Inflation typically leads to higher mortgage rates as lenders adjust to the increased cost of borrowing.

What strategies can borrowers employ to counter the effects of inflation on mortgage payments?

Borrowers can consider refinancing to lock in lower rates or opt for fixed-rate mortgages to shield themselves from inflation-induced fluctuations.

Why is forecasting mortgage rate trends challenging in an inflationary environment?

Inflation introduces uncertainty and volatility, making it difficult to predict how mortgage rates will move amid changing economic conditions.